How do you calculate DV01 of a spread?

The formula of a spread DV01 is: Spread DV01 = – (Δ MTM), for 1 bp in credit spread. A positive spread DV01 means that the CDS position will shed value in response to a 1 basis point upward shift in the CDS seller’s spread curve.

What do credit spreads indicate?

The credit spread is the difference in yield between bonds of a similar maturity but with different credit quality. Spread is measured in basis points. Typically, it is calculated as the difference between the yield on a corporate bond and the benchmark rate.

What happens when credit spreads tighten?

Credit spreads widen (increase) during market sell-offs, and spreads tighten (decrease) during market rallies. Tighter spreads mean investors expect lower default and downgrade risk, but corporate bonds offer less additional yield. Wider spreads mean there is more expected risk alongside higher yields.

How do you hedge the credit spread risk?

Another great method you can use to hedge your credit spread involves purchasing an in-the-money option that has the same expiration as your credit and a delta equal to two or three times that of the net delta of the position.

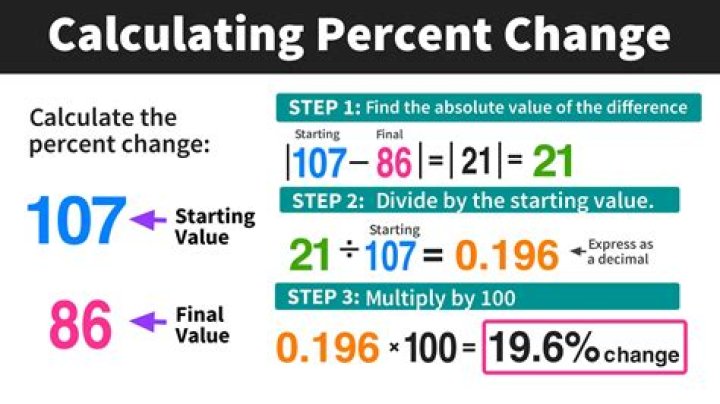

How do you calculate PV01 in Excel?

How do you find PV01 for Bonds on excel

- =pv(rate,nper,pmt,fv) Here,

- PV = Present value. A). YTM (r) = 2.50%/12 = 0.21% (semiannual)

- Substituting the values in formula: PV = (0.21%, 14, 12.5, 1000)

- = $1,143.58. B). YTM (r) = 3.42%/12 = 0.29%

- Substituting the values in formula: PV = (0.29%, 20, 16.25, 1000)

What do widening spreads mean?

The direction of the spread may increase or widen, meaning the yield difference between the two bonds is increasing, and one sector is performing better than another. Widening spreads typically lead to a positive yield curve, indicating stable economic conditions in the future.

What is credit spread risk?

Credit spreads are the difference between yields of various debt instruments. The lower the default risk, the lower the required interest rate; higher default risks come with higher interest rates. The opportunity cost of accepting lower default risk, therefore, is higher interest income.

Are credit spreads widening?

Credit spreads often widen during times of financial stress wherein the flight-to-safety occurs towards safe-haven assets such as U.S. treasuries and other sovereign instruments. This causes credit spreads to increase for corporate bonds as investors perceive corporate bonds to be riskier in such times.

Why are widening credit spreads bad?

Lower quality bonds, with a higher chance of the issuer defaulting, need to offer higher rates to attract investors to the riskier investment. The widening is reflective of investor concern. This is why credit spreads are often a good barometer of economic health – widening (bad) and narrowing (good).

When can you sell a credit spread?

The pace of time decay accelerates closer to expiration, so it often makes sense to sell put spreads with no more than 2-3 weeks until expiration.

Do hedge funds use credit spreads?

Credit hedge funds focus on credit rather than interest rates. Indeed, many managers sell short interest rate futures or Treasury bonds to hedge their rate exposure. Credit funds tend to prosper when credit spreads narrow during robust economic growth periods.

What is the difference between PV01 and DV01 of a bond?

Seem to be confused over the difference between PV01 of a bond and DV01 of the bond. PV01, also known as the basis point value (BPV), specifies how much the price of an instrument changes if the interest rate changes by 1 basis point (0.01%). DV01 is the dollar value of one basis point change in the instrument.

What is the meaning of the pvp01 value?

PV01 refers to present value of 1 basis point and it’s the discounted value of the cashflows for a rate of 0.01% for all periods of a particular instrument, ie, the npv of the fixed leg with a rate of 0.01%

What happens to PV01 when swap rate changes?

When the swap is at fair value (NPV = 0), the two are very very close although not exactly the same, but they will be different and ever more so for non zero NPVs. For given set of market data, changing the swap rate will not change the PV01 but will change the DV01.

What is BPV and hedge ratio?

BPV characterises a price change in the instrument as a result of a basis point change in interest rates. Having calculated the BPV of each of the instruments in a strategy, the ratio of BPVs will determine the appropriate number of contracts to trade or size of exposure to each instrument. This ratio is termed the Hedge Ratio.